Are you looking for a personal loan but worried your fair credit score might hold you back? You’re not alone, and the good news is, fair credit personal lenders understand your situation.

They offer loan options tailored to people like you—those with credit scores that aren’t perfect but still deserve fair chances. Imagine getting the funds you need quickly, with clear terms and no hidden surprises. You’ll discover how to find the best fair credit personal lenders, what to expect from the process, and smart tips to improve your chances of approval.

Keep reading to unlock the door to better borrowing opportunities and take control of your financial future today.

Fair Credit Personal Loans

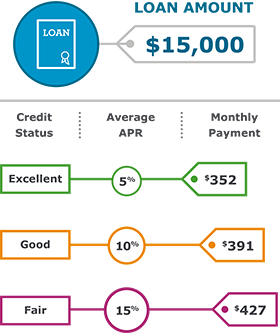

Personal loans for fair credit come in two main types: secured and unsecured. Secured loans require collateral, like a car or savings account, which lowers risk for lenders. Unsecured loans do not need collateral but often have higher interest rates. Loan amounts usually range from $1,000 to $35,000, depending on the lender and your credit profile. Terms can last from one to seven years. Shorter terms mean higher monthly payments but less total interest. Longer terms lower monthly payments but cost more overall. Many lenders offer flexible repayment plans to fit your budget. Understanding these options helps you choose a loan that meets your needs and ability to pay.

Choosing The Right Lender

Banks usually have strict rules but offer stable rates. They may require a higher credit score for approval. Credit unions are member-owned and often have lower rates and fees. They tend to be more flexible with fair credit borrowers.

Online lenders provide quick applications and faster decisions. They often accept a wider range of credit scores but may charge higher interest rates. Comparing all three types helps find the best fit for your needs.

| Lender Type | Approval Ease | Interest Rates | Fees | Processing Speed |

|---|---|---|---|---|

| Banks | Moderate | Low to Moderate | Low | Slow |

| Credit Unions | Easy to Moderate | Low | Low | Moderate |

| Online Lenders | Easy | Moderate to High | Moderate to High | Fast |

Application Process

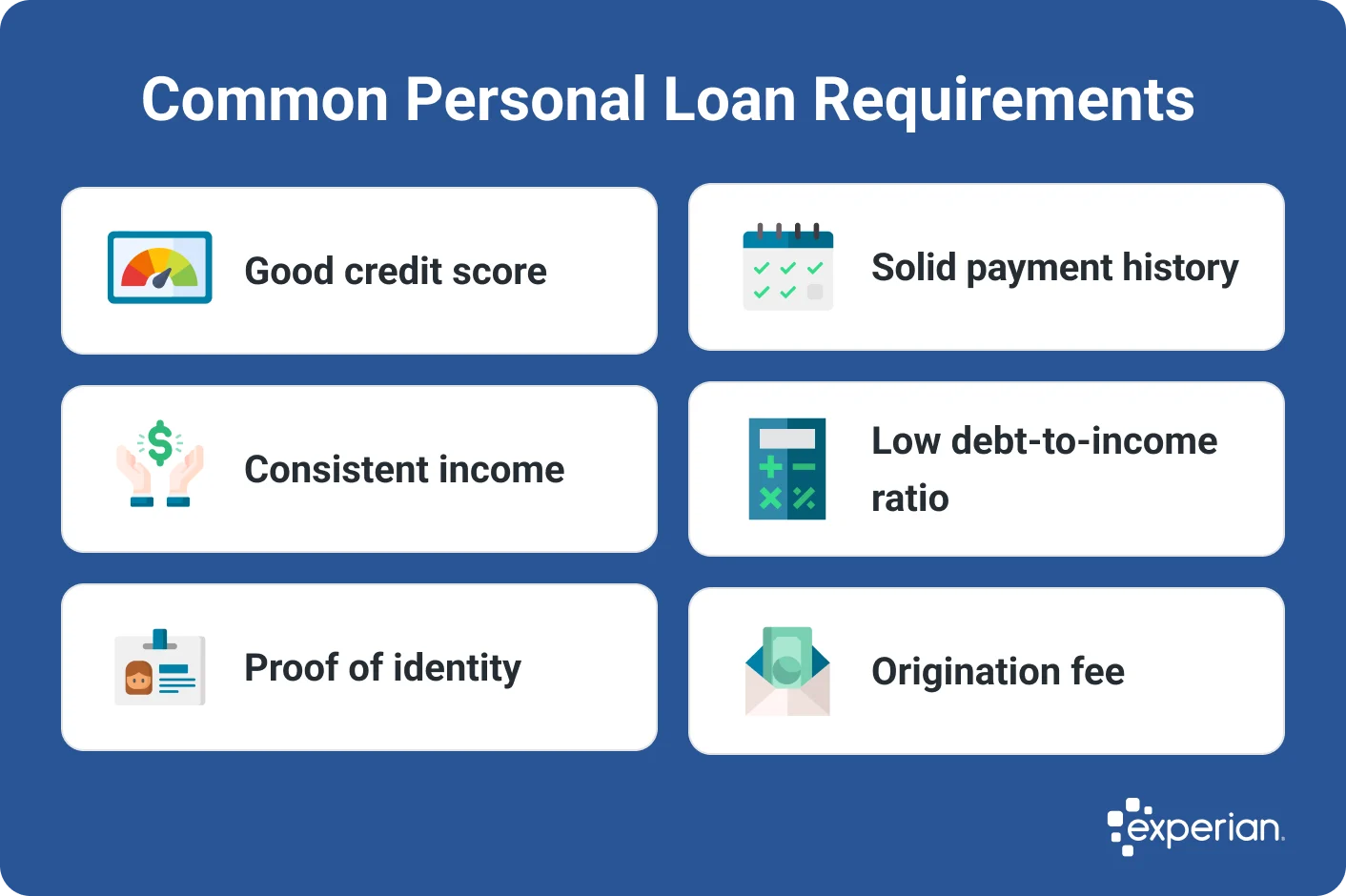

Most lenders require borrowers to be at least 18 years old and have a steady income. A fair credit score usually means a score between 580 and 669. Some lenders may ask for proof of residency and a valid government ID.

Commonly requested documents include a government-issued ID, recent pay stubs, proof of address, and a social security number. Bank statements might also be needed to verify income and expenses.

Applying online involves filling out a simple form with personal and financial information. Upload required documents securely and review the application before submitting. Approval can take a few minutes to a few days, depending on the lender.

Speed And Approval

Same-day loan approvals speed up access to funds. Many lenders use quick online checks. This helps borrowers get fast answers without waiting.

To increase approval chances, keep your credit report clean and provide complete documents. Show steady income and avoid applying for many loans at once. These steps make lenders trust you more.

After applying, expect a quick response by phone or email. Lenders may ask for extra information. Approval means you can review loan terms before signing.

Interest Rates And Fees

Typical interest rates for fair credit borrowers usually range from 12% to 25%. These rates depend on the lender, loan amount, and credit history. Some lenders may offer lower rates if other factors are strong.

Common fees include origination fees, late payment fees, and prepayment penalties. Origination fees can be 1% to 6% of the loan amount. Late fees vary but often add extra costs if payments are missed. Prepayment penalties charge borrowers for paying off loans early.

| Fee Type | Description | Typical Cost |

|---|---|---|

| Origination Fee | Fee for processing the loan | 1% – 6% of loan |

| Late Payment Fee | Charged if payment is late | Varies, usually fixed amount |

| Prepayment Penalty | Fee for paying loan early | Varies by lender |

To compare loan offers, check interest rates, fees, loan terms, and total cost. Look at the Annual Percentage Rate (APR) to see the full cost of borrowing. Read loan agreements carefully. Ask questions if terms are unclear.

Repayment Options

Flexible repayment plans let borrowers choose schedules that fit their budgets. They may offer weekly, biweekly, or monthly payments. This helps avoid missed payments and reduces stress.

Some lenders allow early payments without penalties. This saves money on interest. But others charge fees if you pay off the loan too soon. Always check the terms before agreeing.

Managing loan payments is easier with reminders and automatic transfers. Staying on time improves credit scores. It also builds trust with lenders, helping with future loans.

Loans On Ssdi And Special Cases

SSDI recipients can often qualify for personal loans, but rules vary by lender. Many lenders require proof of income, and SSDI benefits count as stable income. Some lenders may ask for additional documents to verify income and financial status. It’s important to check eligibility criteria carefully.

Loans can be used for business or personal needs. Business loans may require extra paperwork like business plans or financial statements. Personal loans usually have simpler requirements and can cover expenses like medical bills, home repairs, or education.

Fair credit loans help those with bad credit get needed funds. These loans often have higher interest rates and smaller amounts. Borrowers should compare offers to find the best terms. Responsible borrowing and timely payments can improve credit scores over time.

Benefits Of Fair Credit Loans

Building credit history is a key benefit of fair credit loans. Making timely payments helps improve your credit score over time. This can open doors to better loan options later. Fair credit loans often report to credit bureaus, which is important for credit building.

Fair credit loans provide access to emergency funds. They can help cover unexpected expenses like medical bills or car repairs quickly. This support reduces stress during tough financial times.

These loans also assist in improving financial stability. They offer manageable monthly payments that fit your budget. Consistent payments show lenders you are responsible, which can lead to better financial opportunities.

Common Misconceptions

Many believe fair credit loans always have high interest rates. This is not true. Interest depends on many factors like income and loan type. Some lenders offer competitive rates even for fair credit.

Another myth is that approval is impossible with fair credit. Many lenders consider other details like job stability and debt. Approval chances increase with a steady income and good repayment history.

Predatory lenders often target borrowers with fair credit. They use hidden fees and very high interest rates. It is important to read all terms carefully and avoid loans that seem too costly or unclear.

| Myth | Truth |

|---|---|

| Fair credit means high rates | Rates vary; many lenders offer fair rates |

| Approval is unlikely with fair credit | Approval depends on income and history too |

| All lenders are trustworthy | Watch out for predatory lenders and fees |

Resources And Tools

Personal loan calculators help estimate monthly payments and total interest. Use them to compare loan options easily. They show how loan amount, interest rate, and term affect payments.

Credit score improvement tips include paying bills on time, keeping balances low, and avoiding new debt. Checking your credit report for errors can boost your score. Small steps lead to better credit health.

| Customer | Review |

|---|---|

| Kayla | “Easy and fast process, Kayla explained everything well.” |

| Brian | “Brian got my loan approved fast.” |

| Business Owner | “He got my business much cheaper funds than before.” |

Frequently Asked Questions

What Is The Best Personal Loan Company For Fair Credit?

Discover, Upstart, Avant, and Patelco Credit Union rank among the best personal loan companies for fair credit. They offer flexible terms, competitive rates, and quick approvals. These lenders cater to fair credit borrowers with transparent processes and reliable customer service.

Can You Get A Loan On Ssdi?

Yes, you can get a loan on SSDI, but lenders consider your income and credit history carefully. Some specialize in loans for SSDI recipients.

Which Lender Is Easiest To Get A Personal Loan From?

Lenders like Upstart, Avant, and OneMain Financial offer easy personal loans with fast approval, even for fair credit. Online applications speed up the process.

Who Is The Easiest Lender To Get A Loan From?

Discover, Upstart, and Avant are among the easiest lenders to get a loan from. They offer fast approval and flexible credit requirements.

Conclusion

Finding fair credit personal lenders can improve your financial options. These lenders offer loans with reasonable terms and rates. They help people with less-than-perfect credit access funds. Compare offers carefully to choose what fits your needs. Always read the loan terms before signing anything.

Responsible borrowing builds credit and opens more opportunities. Fair credit loans can support your goals without high costs. Take your time and find a lender you trust. Your financial future can get stronger with the right loan.

Read More

- First Time Home Buyer Lenders: Top Tips for Easy Approval

- Remortgage Lender Comparison: Top Tips to Save Big Today

- Top Rated Loan Providers: Trusted Choices for Smart Borrowers

- Specialist Mortgage Lender Quotes: Unlock Best Deals Fast

- Flexible Repayment Loan Offers: Unlock Stress-Free Borrowing Today

- Small Business Lender Quotes: Unlock Best Rates Today

- Equipment Financing Lender Rates: Unlock the Best Deals Today

- Private Mortgage Lender Rates: Unlock Best Deals Today

- Direct Lender Loan Quotes: Get Fast, Low-Rate Offers Today

- Low Deposit Mortgage Lenders: Top Picks for Easy Home Buying