Are you ready to turn your business idea into reality but worried about where the money will come from? Finding the right startup business loan provider can make all the difference in getting your venture off the ground.

Whether you’re just starting out or looking to grow quickly, the right loan can fuel your progress without overwhelming your finances. You’ll discover trusted lenders, smart loan options, and insider tips to help you secure funding with confidence. Keep reading to find the best startup business loan providers that fit your unique needs and set your business up for success.

Top Startup Loan Providers

SBA-backed lenders offer loans guaranteed by the government. They usually provide lower interest rates and longer repayment terms. These loans are great for startups with a solid plan but limited credit history. The application process can take time but is worth the effort.

Community Development Financial Institutions (CDFIs) focus on helping small businesses in underserved areas. They provide personalized service and flexible lending options. CDFIs often support startups that traditional banks may reject.

Regional banks and credit unions offer local business loans. They understand the community and can provide tailored advice. Their interest rates might be competitive, and they often have a simpler application process.

Online lending platforms provide fast access to funds. They usually have less strict requirements but higher interest rates. Startups needing quick cash may find these platforms useful. Many offer user-friendly websites and quick approval decisions.

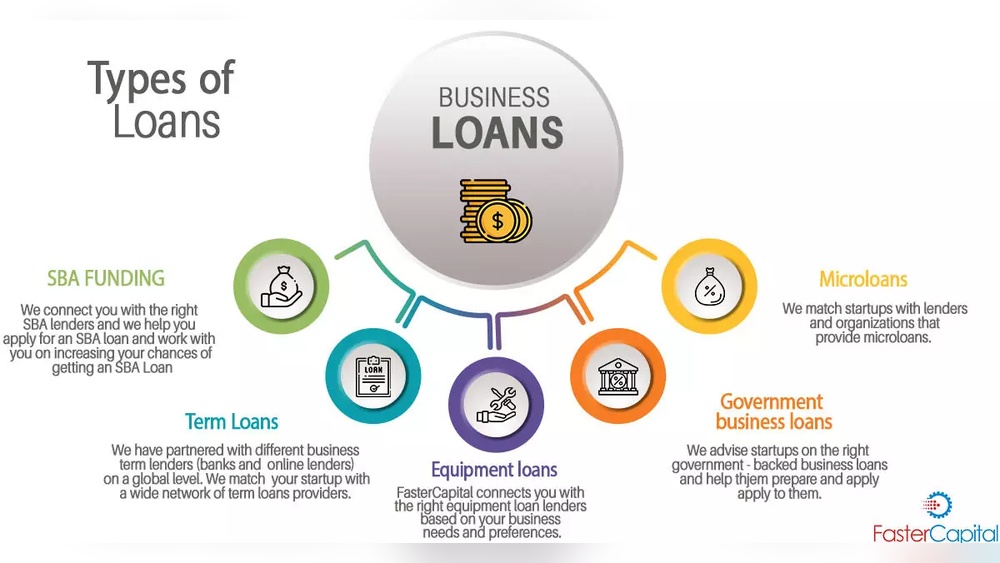

Loan Options For Startups

SBA Startup Loans are backed by the U.S. government. They offer low interest rates and longer repayment terms. These loans help new businesses get funding with less risk for lenders. The application process might take longer but the benefits are worth it.

Term Loans provide a fixed amount of money upfront. You repay it over a set time with interest. These loans are good for buying inventory, marketing, or expanding. They have predictable monthly payments, making budgeting easier.

Business Lines of Credit let you borrow money as needed, up to a limit. You only pay interest on the money used. This option is flexible for managing cash flow or unexpected expenses. It works like a credit card but with lower rates.

Equipment Financing helps buy or lease machines and tools. The equipment itself acts as collateral. This loan type spreads the cost over time, so it doesn’t hit your cash flow hard. Ideal for startups needing costly equipment upfront.

Qualifying For A Startup Loan

Credit requirements often include a good credit score and a clean history. Lenders want to see you can manage money well. A strong business plan shows how you will use the loan and pay it back. This plan should explain your goals and how you will make money.

Collateral means something valuable you promise to the lender. This can be property or equipment. It helps reduce the lender’s risk. Sometimes, a personal guarantee is needed, which means you promise to repay the loan personally.

Revenue expectations are about your business income. Lenders want proof you can earn enough to cover the loan payments. Even startups need to show some expected income or cash flow.

Fast Funding Strategies

Pre-qualification helps save time by showing your loan chances upfront. It needs basic info like credit score and income. This quick step avoids hard credit checks and keeps your score safe.

Online applications offer speed and ease. You can apply anytime, anywhere with just a few clicks. Many lenders provide instant decisions, cutting down wait times drastically.

Local lenders know your community and business needs well. They often provide personal service and flexible options. Building a relationship with them can improve approval odds.

Alternative data includes things like utility payments or rent history. Lenders use it to assess creditworthiness beyond traditional credit scores. This helps startups with limited credit get loans.

Loans For Challenging Credit

Options for startups with bad credit include several loan types. No revenue loan programs help businesses without income statements. These loans focus more on business plans and potential. Guaranteed approval loans promise acceptance but may have higher costs or stricter terms.

Improving loan approval chances requires simple steps. Keep your personal credit clean and pay bills on time. Prepare a clear business plan explaining your goals and expenses. Providing collateral or a co-signer can also help lenders trust your loan request.

Loan Providers Near Austin, Texas

Local banks and credit unions in Austin offer tailored loans for startups. They often provide lower interest rates and personal service. Building a relationship with them can improve loan approval chances. These institutions understand local market needs well.

State and community programs provide funds and support for new businesses. Programs like grants, low-interest loans, and training help startups grow. The Texas government and Austin community both have resources available. These options often have flexible terms for new entrepreneurs.

Specialized startup lenders focus only on young businesses. They offer quick decisions and loans designed for startups’ unique needs. These lenders might have higher rates but easier qualification rules. They help companies without long credit histories.

Networking and business support groups in Austin connect startups with lenders. Local chambers of commerce and business hubs often share loan info. Meeting other entrepreneurs can lead to loan referrals and advice. These groups also offer workshops on financing options.

Frequently Asked Questions

Can I Get A Loan If I Just Started My Own Business?

Yes, startups can get loans through SBA programs, community lenders, or banks offering flexible options. Strong plans and credit help.

What Is The Best Loan For A Startup Business?

The best loan for a startup business is an SBA loan. It offers low interest rates, flexible terms, and supports growth. Other options include business lines of credit and microloans from local lenders or banks. Choose based on your credit, funding needs, and repayment ability.

Can A Start-up Llc Get A Loan?

A start-up LLC can get a loan by proving a solid business plan and creditworthiness. SBA loans and alternative lenders often support new LLCs.

Can I Get A Loan For A Start-up Business?

Yes, you can get a loan for a start-up business. Many lenders offer loans tailored for new businesses. Explore SBA loans, bank loans, or alternative lenders. Prepare a solid business plan and financial projections to improve approval chances.

Conclusion

Choosing the right startup business loan provider matters a lot. Different lenders offer various loan types and terms. Consider interest rates, repayment plans, and fees carefully. Some lenders specialize in new businesses or startups. Government-backed loans can provide extra support and lower risks.

Prepare your documents and business plan well before applying. Taking time to research improves your chances of approval. A good loan can help your business grow steadily. Keep your goals clear and borrow only what you need. Success starts with smart financial decisions.

Read More

- First Time Home Buyer Lenders: Top Tips for Easy Approval

- Fair Credit Personal Lenders: Unlock Fast, Trusted Loans Today

- Remortgage Lender Comparison: Top Tips to Save Big Today

- Top Rated Loan Providers: Trusted Choices for Smart Borrowers

- Specialist Mortgage Lender Quotes: Unlock Best Deals Fast

- Flexible Repayment Loan Offers: Unlock Stress-Free Borrowing Today

- Small Business Lender Quotes: Unlock Best Rates Today

- Equipment Financing Lender Rates: Unlock the Best Deals Today

- Private Mortgage Lender Rates: Unlock Best Deals Today

- Direct Lender Loan Quotes: Get Fast, Low-Rate Offers Today